12th Jun 2020

20 ways to secure your financial future for the next 20 years

Regardless of whether you’ve just started your first crew job or are planning to leave yachting, it’s never too early or too late to take control of your financial future. The following are our top tips to help you take control by managing, growing and securing your money.

1. Review your current expenses

Before deciding how much you can save and direct toward your financial goals, you need to know how much you’re spending. Make it a habit to regularly review your spending and work out if you can save more. An honest appraisal of how much you spend is the best way to start assessing where you’re at financially.

2. Use an app to track your spending

We are never far away from our phones, so one of the best ways to track your spending is via an app. Savings apps can also help you understand how you currently manage money and make suggestions for how you can improve. Being able to track your spending will help you make better decisions and hopefully save more in the long term.

Most apps also come with features that allow you to actively plan your finances, such as setting budgets in different currencies, which is a great feature for Superyacht crew. When you have access to your bank accounts, credit cards, savings and investments in one place, you have a complete picture of your financial life.

Some of the best and most intuitive money management apps we’ve come across include Good Budget, You Need a Budget, Wallet, Joy, Mint and Albert. However, whichever app helps manage your finances, the main objective is developing and sticking to good habits related to money management and savings.

3. Decide what is a want and what is a need

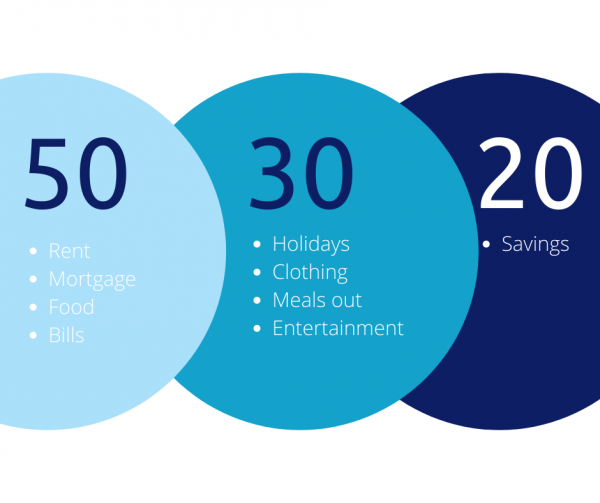

There are things you need, like food and clothing, while others you just want, like the latest smartphone or designer watches. You can fit both into your budget and still set money aside for emergencies if you carefully manage your spending. To start, write a list of everything you spend money on and divide the list into needs and wants. Once you tally the totals, calculate the percentage of each.

The popular ‘50/30/20 rule’ is an easy budgeting method that can help you to manage your money effectively. The basic rule of thumb is to divide your monthly after-tax income into three spending categories: 50% for needs, 30% for wants, and 20% for savings, or paying off debt. By keeping your expenses balanced across these three main categories, you’ll be wiser about your spending habits, and avoid overspending. And with only three major areas to track, it will be easier to stay on track to reach your financial goals.

4. Set a savings goal

After learning how to manage your money and track your spending, set some financial goals. Think about setting goals specifically related to your personal circumstances. If you don’t have anything specific in mind, you will find it difficult to motivate yourself to keep saving and investing every month. Take the time to set realistic financial goals. For many crew members, it starts with a savings plan.

Don’t have your goals written down? Take the opportunity to do it now as it will help to give you some sense of control over your financial situation. Having everything written down in a documented financial plan will help you to avoid making fear-based decisions. It will also help you to measure your progress over time and keep you on track when you’re working toward a long-term goal like buying property or starting a business when you move back onshore.

5. Save regularly

The only ‘right’ time to start saving is now. Regardless of how much you can save every month, saving regularly is key to building your personal wealth. Yachting presents an incredible opportunity to save, but you need to do so in a way that makes sense to you. The amount you can realistically save every month should be based on your income and your expenditure.

One of the most important things you should do as part of your savings plan is build your emergency fund. As well as acting as a financial safety net, an emergency fund can prevent you from spending your money on a whim and instead help you build savings easily without noticing. Therefore, don’t use your day-to-day bank account for your emergency money.

Also, consider whether you can commit to a longer term, regular savings plan. Committing to a regular savings plan essentially means agreeing to tying up your money for a period of anywhere from 5 to 20 years. As with any finance-related decision, there are pros and cons of committing to a regular savings plan.

The most important thing is to analyse your current spending and determine what’s actually stopping you from saving before you launch into choosing the best savings options for you. And the sooner you build the habit for saving, the better your savings-potential over time. Check out our free Yachties Guide to Saving for more tips on how to become a super saver.

6. Make compound interest work for you

Compound interest refers to a method of continually reapplying interest to a principal (the original sum of money put into savings or an investment) that is growing over time. This calculation of interest is present on virtually all credit card and loan payments where a debt grows with each unpaid billing cycle. That’s when compound interest works against you. However, it can work to your advantage when applied to your savings or investments.

Put simply, compound interest is interest on interest, which is a powerful financial force when allowed to accumulate over a long period of time. Compound interest puts your hard-earned money to work and grows larger as it feeds on itself.

The good news is you don’t need to start with large amounts of money. Whatever amount you can afford to put away in a savings account, the longer you let interest compound on itself and the more dramatic your gains will be. Use compound interest to your advantage and make your savings work harder.

7. Find a savings buddy

Ever noticed how much easier it is to achieve your fitness goals when you agree to meet a friend for a workout? The same principle can apply to your finances. If you have a reliable and trustworthy friend or family member you know can help you reach your financial goals, make them your savings buddy. Sharing your savings goals with people you trust can help keep you accountable and increase the chance of you reaching those goals.

It could be as simple as sharing that you want to save €5,000 in the next six months. To do that, you need to save €200 a week. Every week, you check in to confirm whether you put the money aside. If you didn’t, you will soon realise that it’s easier to save the money than admit to spending and not achieving your goal! In yachting, it’s especially easy to be pressured into spending when your expenses are low and cash flow is high. Having someone who understands what you want to achieve will help curb the temptation to constantly spend and also make you feel less alone in your efforts.

8. Change your credit card

If you owe a large amount on a high-interest credit card, it will be more challenging to pay it off quickly. Monthly charges can eat into your minimum payment, so you see only small, incremental changes. Try asking your bank or credit card provider for a lower interest rate or look at transferring the balance to a low-interest rate credit card. A few months of interest-free payments may be all it takes to pay off your balance, which means you can redirect that money towards your savings. If it’s not possible to switch cards, pay as much as you can every month. That is, always try to pay more than the minimum monthly amount if you want to make real progress towards paying off high-interest debt.

9. Keep an eye on bank interest rates

If you’re a borrower, the interest rate is the amount you are charged for borrowing money – a percentage of the total amount of the loan. If you’re a saver, it’s the same except the interest is paid to you.

Whether you’re borrowing or saving, interest rates can be confusing but the most important thing to know is that even a small change in interest rates can have a big impact. It’s important to keep an eye on whether they rise, fall or stay the same. More importantly, understand how a change in interest rates could impact your savings and loans.

10. Pay off your debt as quickly as possible

This is one of the most important things to do to get ahead financially. List all of your current debts, including credit cards and personal loans, and work out the minimum amount you must pay. Then evaluate your expenses and determine how much more you could pay towards repaying your debts. If you’re paying only the minimum amount every month, it will take you much longer to clear your debt. Also try consolidating multiple debts into one and always look at your spending habits and adjust them if necessary, to pay off debt as quickly as possible.

11. Get to grips with assets and liabilities

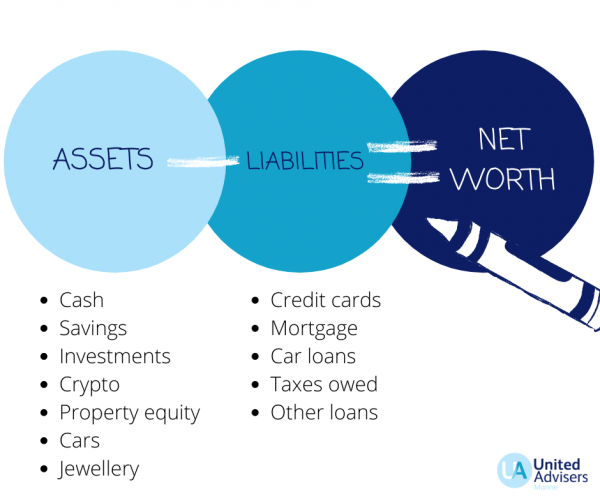

An increasingly popular way to understand how financially healthy you are is to know your net worth. Net worth is simply the value of all your assets (what you own) minus all your liabilities (what you owe). Assets include everything from cash, money in your savings accounts to vehicles and property. Liabilities include any money you owe in the form of loans, credit card debt or mortgages. In theory, your net worth is the value in cash you would have if you were to sell everything you own and clear your existing debt.

If your assets exceed your liabilities, you have positive net worth. If your liabilities are greater than your assets, you have negative net worth. If you track your net worth over time, it will show whether you are making progress toward your financial goals. It will give you a clear idea of whether you are spending too much, how much you have in savings and whether you’re putting enough away for retirement.

12. Build a passive income

There are two main ways to making money: earning it actively by working for a salary or earning it passively, by saving or investing in stocks, real estate or other savings vehicles such as investment platforms. To help secure your financial future, look for opportunities to generate income on the side. Passive income from a rental property is another way to build wealth or find extra money to help pay off debt.

13. Contribute towards your pension

Regardless of whether you’re nearing retirement or just starting to plan your future, saving for later in life is essential. It makes good financial sense to think carefully about what you wish to do once you leave yachting, whenever that may be.

There are a few different factors to consider such as your ideal retirement age and what exactly a “comfortable” retirement means to you when you’re back on shore. Whatever you have in mind, you need to plan ahead and be honest about how much you need to save. This is especially important if your employer doesn’t contribute towards a pension.

In our Crew Financial Wellbeing Survey, only 6% of respondents said that their employers contribute to their personal pensions. That figure is low when compared to other industries, especially those based onshore. We also know from speaking with crew that many don’t feel supported enough when saving towards their retirement.

Yachting presents an incredible opportunity to build personal wealth with its high wages and reduced costs while working and living onboard. By putting aside regular amounts of money now, you can amass your own form of pension-like savings.

14.Protect yourself with the right insurances

Protect your finances by having insurances in place and ensure they cover the right things should something unexpected happen. When it comes to onboard accidents and illness, what you’re covered for varies depending on the conditions stipulated in your contract. Your employer may not always provide health insurance and, if so, their policy may not offer cover during probationary periods. Always review your contract carefully.

If you own property, make sure you have the appropriate homeowner’s insurance and renter’s insurance if necessary. A surprisingly high number of people are tempted to skimp on insurance but keep in mind that having it protects you from potential catastrophes that can create a sinkhole in your best laid financial plan.

15. Use exchange rates to your advantage

Currencies continuously fluctuate and if you can secure a good exchange rate, you will make your cash go a long way. To get the best rates while abroad, be sure to always use credit and debit cards that do not charge an international transaction fee. If your credit card has no international transaction fees, paying in the local currency can give you the best exchange rate at the point of purchase without additional hidden fees tacked on. Increased popularity of online banking and a much more flexible foreign exchange market has given rise to a larger range of bank accounts available to Superyacht crew, so consider your options and use exchange rates to your advantage.

16. GET the right account

We’ve met a number of crew, especially at the start of a season, who had their hard-earned cash sitting in bank accounts or under their mattress making 0%. They figured that everything was fine. Unfortunately, those same crew received quite the shock when, at the end of the season, they realised they’d missed a valuable opportunity to make their savings work harder. Imagine how much happier they would have been coming back to shore and being faced with greater savings just because they made a simple switch of bank accounts. Always review your bank accounts and make sure they meet your needs.

17. Make the most of your DINK status

When you have a higher disposable income it’s easy to fall into the trap of spending more than you save. Nothing should prevent you from enjoying what you earn but just make sure you aren’t frittering it away at the expense of saving for your future. It’s about making the right decisions today that develop healthy savings and investment habits.

If you are a DINK (Double Income No Kids), you are part of a group that has the biggest propensity to save and explore more investment opportunities. Perhaps you could even live off one income and save the other. The so-called ‘50% lifestyle’ has become popular with those who have the financial flexibility to support it. It isn’t a solution for every couple, but it’s a method of re-organising spending and saving that’s growing in popularity.

18. Join a FIRE community

There’s a growing movement of people who are practicing FIRE (Financial Independence Retire Early) principles and retiring up to 10 years earlier than traditional retirement age. Some refer to FIRE as the ‘ultimate life hack’.

Ambitious, often middle-income earners are using the following formula to reach financial independence sooner: high savings rates (50–70% of their incomes) + frugal living (minimalism) + low-cost stock index fund investing.

While not everyone who follows the formula embraces traditional retirement, the milestone for having reached financial independence is the moment when what they earn from investments pays for their expenses. According to FIRE adherents, when you hit that tipping point, the choice to work or not is yours and you are in control of how you spend your time.

19. Improve your financial awareness

Understanding your finances seeps into every area of your life regardless of whether you think it does or not. That’s why it’s important to understand things like personal finance, borrowing, saving and investing. Being financially literate allows you to make more informed decisions and manage your money more effectively. Learn as much as you can about things like credit, saving and investing, which will also help you to become. Also, the disciplined about your money habits and make decisions about your future.

Be sure to check out our resources, written specifically for Superyacht crew, to help you learn more about managing your money and planning for your future.

If you have any questions about our tips or finance in general, please contact us.

20. invest in yourself

Staying competitive in the workplace is important to your overall financial health. How? By constantly improving your skills and industry knowledge, you’re putting yourself in a better position for a promotion on board a yacht. Look for opportunities to pursue additional certifications that will increase your earning potential and qualify you for more advanced crew positions. The skills you learn will also certainly help for your life after yachting.